As the seasons changed and their lives continued to evolve, John and Kayla found themselves embarking on a new chapter: parenthood. With the joyous news of their impending arrival, they felt a newfound sense of responsibility to provide a stable and nurturing environment for their growing family. After careful consideration, they realized that the time had come to take the leap into homeownership.

With diligent saving and prudent financial planning, John and Kayla had managed to amass enough funds to make a down payment on a starter home. Excitement mingled with trepidation as they delved into the nuances of buying a home in the 1980s.

Determining their budget became the first order of business, with John and Kayla meticulously reviewing their finances to ascertain how much they could comfortably afford to spend on a home. “We knew we had to be realistic about what we could afford,” John reflected, “but we also wanted to ensure we found a place that felt like home.”

Consulting with professionals became paramount, and they sought the guidance of a trusted real estate agent, referred to them by family. Together, they embarked on a series of open house visits, exploring various neighborhoods and considering their options. “We weren’t married to any one town,” Kayla remarked, “but we had a few in mind that we thought would be perfect for starting our family.”

Location played a crucial role in their decision-making process, with Kayla expressing a desire to be close to her parents when their first baby arrived. “Family is everything to us,” she shared, her eyes alight with anticipation. Eventually, they settled on a modest cape cod in Somerset, NJ, with a picturesque backyard that backed up to woods and was just a stone’s throw from a park.

As Kayla transitioned into her role as a paralegal at a local law firm, and with John continuing his career as a chemist, they navigated the complexities of home buying with diligence and determination. “We made sure to cut back on spending during the process,” John recalled, “because we knew that any big purchases could potentially derail the closing.”

Understanding the costs associated with buying a home, such as inspection and appraisal fees, as well as commissions and closing costs, was essential. They recognized the importance of maintaining their credit scores and ensuring they were in good standing to secure favorable lending terms. “Our credit scores played a significant role in determining the interest rate on our mortgage,” Kayla explained, “so we made sure to monitor them closely.”

Special Considerations When Buying a Home:

School District: Considering the quality of local schools is crucial, especially for future family planning.

Commute: Assessing commute times to work and proximity to essential amenities like grocery stores and healthcare facilities.

Neighborhood Safety: Researching crime rates and neighborhood safety statistics to ensure a secure environment for raising a family.

Home Size and Layout: Evaluating the size and layout of the home to accommodate future needs, such as additional bedrooms for children.

Future Growth: Considering the potential for property appreciation and future development in the area.

Home Inspection: Hiring a professional home inspector to assess the condition of the property and identify any potential issues or repairs.

Financing Options: Exploring various financing options and mortgage rates to secure the most favorable terms.

Closing Timeline: Planning for a realistic closing timeline to ensure a smooth transition from renting to homeownership.

Reflecting on their journey, John and Kayla felt a sense of pride and accomplishment as they crossed the threshold of their new home. “Buying this house isn’t just about having a place to live,” John remarked, “it’s an investment in our future and the future of our family.” With hearts full of hope and dreams of what lay ahead, they embraced the next chapter of their lives with optimism and gratitude.

Disclosures:

Investment Advisory Services offered through Retirement Wealth Advisors, Inc. (RWA) an SEC Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Consult your financial professional before making any investment decision.

This information is designed to provide general information on the subjects covered, it is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market, or recommend any tax plan or arrangement. Please note that Professional Planning Services and its affiliates do not give legal or tax advice. You are encouraged to consult your tax advisor or attorney.

Annuity guarantees rely on the financial strength and claims-paying ability of the issuing insurer. Any references to protection benefits or lifetime income generally refer to fixed insurance products. They do not refer, in any way to securities or investment advisory products or services. Fixed Insurance and Annuity product guarantees are subject to the claims‐paying ability of the issuing company and are not offered by Retirement Wealth Advisors, Inc.

In the hustle and bustle of their young married life, John and Kayla encountered an unexpected roadblock as John’s trusty Dotson broke down on his way to work at ABC Pharmaceutical one Monday morning. With a sense of urgency, they were thrust into a situation that demanded quick decisions and careful planning.

Returning home, John and Kayla sat down to assess their options. Kayla, ever the pragmatic thinker, suggested, “Until we can get to a dealership, I’ll drive you to work. It will do for the time being, and we’ll be sure to get something this weekend.” Her calm demeanor provided a reassuring anchor amidst the uncertainty.

As the week progressed, John and Kayla embarked on a journey of research and exploration, visiting various dealerships in the evenings to gain insights into pricing and available options. They knew they had some savings to put down, but they treaded cautiously, mindful not to deplete their emergency fund entirely.

The choice between buying and leasing a car loomed large, each option presenting its own set of pros and cons. Leasing seemed tempting with its lower monthly payments and the allure of driving a newer, more expensive vehicle. However, John and Kayla remained steadfast in their desire to own their car outright, free from the perpetual cycle of payments.

John Sr. and Sarah (John’s parents), wise voices of experience, weighed in on the decision-making process. John Sr. sagely reminded them, “You still have a cost whether you pay cash or finance.” His words resonated deeply with John and Kayla, prompting them to opt for financing a small, reliable car that would eventually be theirs to keep.

Armed with newfound knowledge from the recently acquired Kelly Blue Book, John and Kayla meticulously researched their options, determined to make an informed choice. Financing a new car seemed daunting, requiring a substantial initial outlay of money, but they understood the value of investing in reliability and peace of mind.

On a crisp Saturday morning, John and Kayla embarked on a pivotal journey to their local dealership, their hearts set on securing a reliable vehicle that would fit within their budget. The gleaming 1984 Pontiac 6000 caught their eye, and after careful negotiation, they sealed the deal for a slightly discounted price of $7,999.

“We’ve put down 20% and financed the rest for 36 months,” John remarked, his voice tinged with satisfaction. Kayla added, “It’s a bit of a stretch on our budget, but we’re willing to make sacrifices to ensure John’s safe commute to work.”

With the purchase finalized, John and Kayla felt a sense of accomplishment and relief wash over them. As they drove their new car home, they knew that they had made a decision that would serve them well on their journey together. Through careful planning and thoughtful consideration, they had navigated yet another challenge, emerging stronger and more resilient than before.

Tune in next week to hear what John and Kayla are up to!

Investment Advisory Services offered through Retirement Wealth Advisors, Inc. (RWA) an SEC Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Consult your financial professional before making any investment decision.

Workplace Elections, Building an Emergency Fund & More!

As March paints the world in hues of green and blossoms, John Jr. and his new wife Kayla stand on the precipice of a fresh season in their lives, brimming with excitement and anticipation. With John commencing his career as a chemist at a local pharmaceutical company in NJ, and Kayla diligently balancing her part-time job as a server with her final days as a college student, the couple finds themselves faced with an array of consequential financial decisions.

Sitting down together, John and Kayla meticulously pore over the offerings of John’s new workplace benefits, recognizing the significance of each choice. John, with a furrowed brow, considers the intricacies of health insurance, weighing the merits of an HMO versus a PPO plan. “The HMO offers lower premiums but more out-of-pocket costs, and offers less flexibility in choosing healthcare providers,” he muses, while Kayla nods in agreement, adding, “But the PPO provides more freedom to see specialists without a referral, although the premiums are slightly higher.” John and Kayla check their doctors through the carrier’s provider search and determine that the HMO will work for them for now, as their healthcare needs are low and their doctors are in-network with the HMO.

Their discussion then turns to short-term disability insurance, where John raises questions about the coverage provided. “Short-term disability can be a financial lifeline if I’m unable to work due to illness or injury,” he explains. “But we need to understand the waiting period and the percentage of income it replaces,” Kayla interjects, her eyes reflecting their shared determination to make informed decisions. They ultimately decide to elect the short-term disability while understanding its limitations. It’s low cost, and can help protect at least some of John’s income, so it’s worth it to them.

As they delve into the intricacies of group life insurance, John notes the importance of weighing its benefits against its limitations. “It’s a cost-effective way to secure financial protection for our loved ones,” he remarks, “but we need to remember that coverage terminates if I leave the company.” Kayla nods solemnly, understanding the importance of considering the long-term implications of their choices. They decide to consider individual term insurance for John as well, and eventually Kayla. If the premium is affordable, they may take both. For now, they elect the group life insurance for the low cost and protection it provides now.

Their attention then shifts to the 401k plan, where John grapples with determining the optimal contribution. “The 6% match is enticing,” he reflects, “but we also need to consider our budget and other financial goals.” Kayla nods in agreement, adding, “Perhaps we start by contributing enough to receive the full match, and then anything beyond that, we squirrel away in savings for a downpayment on a home.” They exchange a glance, a shared vision of their future taking shape before them. They’re renting a small place now, but one of their goals is to buy a house near Kayla’s parents so they will have help when they decide to begin a family.

Amidst their deliberations, John and Kayla also contemplate how to best utilize the monetary wedding gifts they’ve received. “Investing in our future is important,” John asserts, “but we also want to ensure we have some liquidity for emergencies.” Kayla nods in agreement, her gaze alight with determination. “Let’s use a portion of the wedding funds to start an emergency fund,” she suggests, “to give us a solid financial foundation.” John and Kayla had heard that it’s important to have 3 to 6 months of expenses in the bank in case of emergency.

As the sun sets on their discussion, John and Kayla feel a sense of empowerment, knowing they’ve approached their financial decisions with diligence and foresight. With spring’s promise of new beginnings infusing their spirits, they embark on this journey together, ready to embrace the opportunities that lie ahead. Their commitment to open and honest financial discussions strengthens their bond, as they navigate the complexities of adulthood hand in hand.

DISCLOSURES:

Investment Advisory Services offered through Retirement Wealth Advisors, Inc. (RWA) an SEC Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Consult your financial professional before making any investment decision.

This information is designed to provide general information on the subjects covered, it is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market, or recommend any tax plan or arrangement. Please note that Professional Planning Services and its affiliates do not give legal or tax advice. You are encouraged to consult your tax advisor or attorney.

Annuity guarantees rely on the financial strength and claims-paying ability of the issuing insurer. Any references to protection benefits or lifetime income generally refer to fixed insurance products. They do not refer, in any way to securities or investment advisory products or services. Fixed Insurance and Annuity product guarantees are subject to the claims‐paying ability of the issuing company and are not offered by Retirement Wealth Advisors, Inc.

MERRY CHRISTMAS and HAPPY NEW YEAR! As the year comes to a close, the team at Professional Planning Services is not only reflecting on the successes and milestones we’ve achieved together but also taking a moment to express our heartfelt gratitude to our valued clients. In addition to our collective accomplishments, we’d like to shine a spotlight on the incredible dedication and personal growth of our team members. Let’s take a closer look at the remarkable journeys of Chris Lester, Katelyn Erchick, Keith Lester, and Alan Fried.

Chris Lester: Nurturing Knowledge and Family

This year, Chris Lester devoted his efforts to expanding his expertise in extended care and later life planning. His commitment to continuous learning led him to achieve designations in long-term care (CLTC®) and Social Security (NSSA®), enhancing his ability to navigate complex later life planning scenarios. Outside the professional sphere, Chris prioritized family and martial arts. His dedication to education will continue into 2024, where he aims to share insights about the innovative platform Currence with friends and clients.

Katelyn Erchick: A Year of Achievements and Adventures

Katelyn Erchick’s journey in 2023 was marked by remarkable achievements and personal adventures. She secured her CLTC® and became an Investment Advisor Representative after successfully passing her Series 65 exam early in the year. On the personal front, Katelyn volunteered at her daughter’s school, explored her favorite island, Aruba, and enjoyed a road trip to Wisconsin, with a memorable stop in Ohio’s Port Clinton. Looking ahead to 2024, Katelyn is eager to explore more of the United States, with the Great Smoky Mountains and Dollywood as the first exciting destination.

Keith Lester: Diving into Growth and Overcoming Loss

Keith Lester’s highlight of the year was a unique and unforgettable experience—swimming with whale sharks alongside his father. He dedicated his time to assisting more health insurance clients than ever before, demonstrating his commitment to helping others. On a sad note, Keith faced the loss of his beloved grandmother and sweet dog this year. As he looks forward to 2024, Keith is excited about more diving adventures and continued growth through certifications and ongoing education.

Alan Fried: Resilience and Light in the Face of Challenges

Alan Fried faced a health scare with his eye after a cruise in 2023 but has since made a full recovery and is back to business. Beyond his professional role, Alan is a shining light as a friend and advisor, contributing positively to the team dynamic. We are grateful to have him as part of our team and look forward to more shared successes in the coming year.

As we bid farewell to 2023, the team at Professional Planning Services extends warm wishes of MERRY CHRISTMAS and HAPPY NEW YEAR to our clients, friends, and colleagues. We are grateful for the trust and support that have defined this year and are excited about the opportunities that 2024 will bring. Thank you for being an integral part of our journey, and here’s to continued growth, prosperity, and shared success in the upcoming year!

Investment Advisory Services offered through Retirement Wealth Advisors, LLC (RWA), a Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Insurance products and services are not offered through RWA but are offered and sold through individually licensed and appointed agents.

A few weeks ago, I came across a strategy that I was unaware of. Because this is happened to me personally, I felt it paramount to do a deep dive on this.

I don’t like to promote products but rather educational topics. However, being in the financial arena, we do need to explore specific products from time to time to understand how they work in order to make informed decisions.

The first thing I want to mention is a very great loss in my family: my dad’s older brother, my uncle Ron passed away on Wednesday. It’s sad. He was one of the men in my life that helped shape me into who I am. My dad, most of you did not know. My father was born with retinal glaucoma. Cancer of the eyes. He was blind in one eye and their mother, Tub, my grandmother, was challenged as a registered nurse to raise three boys as a single mom. Not only did she raise three boys, but her middle son was also handicapped.

My dad passed away about 20 years ago, but during my life what I always knew was that my dad’s brothers were always there, and they were cut from a cloth that I don’t see much of any more.

Uncle Ron was a husband, a father to my cousin Jimmy who was adopted first, and then he was able to bear two other children, Holly and Brock, who he was very proud of. He had a Virginia license plate “DOCnJOCK.” My uncle was the jock, his wife the doctor. He was all state in Florida before he became a Navy seal. Played football, loved football. He got out of the military and went to work for the high school, he then committed and supported his wife, my aunt, while she got through medical school and become an MD. I truly believe that had my Aunt Barb not been a part of his life my Uncle Ron would’ve passed much sooner. It was her or medical awareness that kept him as healthy as he could be. He was also a brother to my dad and my uncle Dave, the youngest. He was a high school football coach. He just showed me and gave me a lot of character.

I will truly miss him. Until we meet again. I do not believe it’s final, I do believe that we move on to other things unknown.

But the reality is while we are here, we must plan. Do you know who paid for Princes’ funeral? The man was worth 156 million dollars, and his family had to borrow money to bury him. George Lopez the comedian gifted Princes’ family $20,000 to cover those costs. Now why does the family of a man who was worth so much not have the money to pay for his celebration of life?

When I was down in Kentucky recently, I met this gentleman that was sharing this information with me, I started to think back. Some of you know I lost an advisor and friend who I mentored in South Carolina last year. He was 57 years old and had a tree fall on him when he was working on his farm. Freak accident. Since it was during Covid and because he was his own advisor who wrote his own policies, one of the things that stood out to me was when his spouse called me who I had never met, never spoken to before, asking for my help to decipher this information.

She started to send me documents from different insurance companies, brokerage accounts, all this stuff. On the surface, you say, “he had life insurance, he had death benefits, he had money in the bank…” but a lot of this stuff was tied up in his name. What I realized at that point in time is that the immediate moment, like my uncle Ron who just passed away on Wednesday, the family’s going to need cash. Now if you’re married and you have cash and you have a joint checking account, money is available.

Typically there’s some money and funds set aside. But it’s at the loss of the other spouse that things can get squirrely. It took seven months for the medical examiner to issue a death certificate with the cause of death to the spouse of my friend Jeff. You would think, natural causes, tree fell on you, how difficult could it be? But because it was such a freak accident, because of Covid, it took a long time.

You may say, that’s a rare circumstance. So this gentleman started to share some statistics on how long it takes to get a death certificate across the nation, and we went and pulled New Jersey’s processing time and saw that New Jersey is 4-6 weeks if you file online to get a death certificate. That’s what you need in order to get access any funds – a death certificate. You can go downtown to East State Street in Trenton for same day processing, but good luck with that. Governments are short-staffed and overwhelmed.

When I was in Kentucky the statistic he shared with me, in Texas it’s taking 25 to 30 days.

Most people think they can access dollars upon the death of their family member through their life insurance policies or annuities. But what became evident to me, if these companies don’t have a death certificate, if there is an issue where there it was not a definitive cause of death, they will not be able to pay the claim until they have that information. If the death certificate you get says “cause of death unknown,” you’re in trouble.

Another thing people think offers them security is a living trust. Say you have bank accounts with TODs (transfer on death) or PODs (payable on death).

Power of attorney. Power of attorney is while they’re alive. After they die, you need to the will, the trust, the executor.

Maybe you’ve thought of final expense insurance.

ALL OF THESE THINGS require a death certificate. And that is a cog, or a fly in the ointment. That’s the challenge.

So that what was appealing to me about Beneficiary Liquidity Plan. Funds that typically people are going to give to the beneficiaries anyway, they can utilize for a single premium guaranteed fixed whole life insurance policy paired with an irrevocable living trust that is payable to the beneficiary on death WITHOUT a death certificate within 24-48 hours of death.

The funds grow tax deferred, that’s not why we’re doing it. The key is that it pays within 24 to 48 hours with just a signature from the funeral home director. We don’t have to borrow funds from the funeral home at probably at above going rates. There are no health questions on the application. Doesn’t matter. As long as you’re not in triple digits.

You wouldn’t set up this plan to get rich or for leverage like traditional life insurance. It is only to make sure that the people that are in her life, that they are not burdened upon your death.

And this is another scenario… you have three children. One child who is the closest who’s taking care of mom or dad says, you know what, you guys are over there, I’ll pony up the money and take care of this for right now and you can reimburse me later. Then it doesn’t happen and now there’s a rift in your family. I’ve always said money makes people funny.

You can setup a plan like this for as little as $2,500. You could do $5,000 one-year, $5,000 the next and stack them together. The max allowable is $100,000.

If you put in $20,000, that’s what your beneficiaries are going to get back. Technically there’s a small death benefit, but it will be something very minimal like $500 or some small amount but that’s not what this is for. Its purpose is creating liquidity for the family at a point in time when they need it. It just takes a lot of the stress that can typically happen off the table.

So how do you fund it? I am setting a client up right now, and he’s divorced, 73. He’s taking RMDs now. And I asked him, are you using those, and he said no, that money goes right in the bank. He has to pay taxes on it next year so we’re setting up a 10% free withdrawal to fund this so that his son who is executor doesn’t have to deal with this nonsense when he passes.

If you got some old contracts, you want to make them liquid. You have an old brokerage account, mattress money. I just had a couple who had money sitting in the bank without interest. We repurposed it to make it liquid for their beneficiaries.

$15,000 is the national average for a funeral, and it’s the same in New Jersey. You don’t have to go nuts here, but it’s just a smart and prudent idea in my opinion to set this up for your beneficiaries.

Investment Advisory Services offered through Retirement Wealth Advisors, LLC (RWA), a Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Insurance products and services are not offered through RWA but are offered and sold through individually licensed and appointed agents.

Annuity guarantees rely on the strength and claims-paying ability of the issuing insurer. Any references to protection benefits or lifetime income generally refer to fixed insurance products. They do not refer in any way to securities or investment advisory products or services. Fixed insurance and annuity product guarantees are subject to the claims-paying ability of the issuing company and are not offered by RWA.

Index or fixed annuities are not designed for short term investments and may be subject to caps, restrictions, fees and surrender charges as described in the annuity contract. Guarantees are backed by the financial strength and claims paying ability of the issuer.

This blog post is a conversation between Chris Lester and Mark Diorio from 5/12/22.

CL: Today I wanted to have a conversation about Cryptocurrency – What is it exactly and is it something that you can add to your portfolio of investments?

To answer these questions, I’ve brought on Mark Diorio – he is the Chief Investment Officer of Brookstone, and a chartered financial analyst (CFA). For those of you that don’t know what that means, in my experience, when I go to meetings or conferences (and I’m sure he’ll sidestep this comment, but I am telling you based on my experience) is that they are usually the smartest people in the room. In Mark’s case, he’s down to earth, salt of the earth. What I really like and appreciate about him is that he doesn’t speak over your head. With that being said, you should understand what he is saying in this conversation.

Source: easycrypto.com

MD: We have a pretty interesting topic that Chris put together, the ABC’s of Cryptocurrency, and I put this easy to read slide together just to give you an idea of a little bit of history of cryptocurrency. That’s a little tongue-in-cheek, but really what our role is, is to kind of decipher. There’s a lot of news headlines, and a lot of it is eye-catching in terms of what is happening and what has happened over the years in cryptocurrency. There’s a lot going on, but our role is not to sell cryptocurrency in that sense, our role is really to advise and cut through a lot of this noise to define what it is, what we see it’s roll as going forward, and does it impact you and would it impact you in any given way.

IN GENERAL

Source: pwc.com

So, let’s just define cryptocurrency really quickly: cryptocurrency in general is considered a medium of exchange. So that sounds like the typical US dollar, which is a currency. The dollar is designed to be a medium of exchange, a unit of account, and a store of value. This is a little bit different, so I don’t want you to think because it has the “currency” name in there, it’s like the currency of a country like the US (or the euro or the Japanese yen…etc.) it’s not like that. It is the currency of the network, and I’ll explain a little bit what that means, but it’s pegged to be used as a currency in the sense of everyday transactions. That’s one of the myths I think that’s out there, and I’ll touch on that a bit too.

But overall, I’d point out that it’s only in digital form. It has no physical form. So, if you see a picture of a gold coin with a “B” in there and it looks like an actual coin, the point is, it doesn’t exist. It’s only in digital format.

One of the benefits and one of the arguments that proponents of cryptocurrency make (Bitcoin, being the original one) is that the supply of Bitcoin, unlike the supply of US dollars or any other traditional currencies is not dictated by the central bank. The federal reserve is the central bank of the US. So, cryptocurrency is really dictated by the terms of the network. In this case, the example we’re going to use is the largest and most well-known cryptocurrency: Bitcoin. The terms of the Bitcoin network tell you how many Bitcoin will be minted over what time period, and that adds to the value that some investors see in it.

TECHNOLOGY

Source: pwc.com

You have to think of cryptocurrency just like any other new technology: there’s some benefits, and some drawbacks. The benefits include increased transparency, you can track things, there’s some cost reductions, just like what you would think with any other technologies. On the other side, there are several unknowns as well. It’s complex technology, regulators don’t know what to do with it because you’re transacting in currency format and making trades, and there’s big moves up and down in valuations. It’s really kind of confusing to wrap your arms around it in a full-scale regulatory environment. I do see that coming, and that’s only going to be to the benefit of both the technology but also the users that may find use cases here.

BLOCKCHAIN

Source: pwc.com

I won’t spend a lot of time on the above graphic because it’s easy to get lost, but if you follow from the top left all the way around, the technology that supports cryptocurrency is called blockchain technology. How it works is, if you send a message or a computer system sends a message that they want to take one cryptocurrency and give it to somebody else, it sends a message to another computer system or network of computers that maintain the ledger. The ledger basically just says who has what.

For example, Chris has 100 Bitcoin, let’s say, and I have 200. Well, if he says he sends me 200, a system will automatically reject that and says, “well you only have 100, you can’t sell 200.”

Usually who would keep that record is a bank. That intermediate third-party who keeps the ledger. Now, what the technology has done is said, “we’re going to keep the ledger amongst a variety of computer systems.” Anyone (it’s open source) can go and see this transaction ledger.

So, the ledger validates all the transactions that occur within a stated time period – let’s say within 10 minutes for Bitcoin. For example, all those transactions get put together in a block, validated, and then put into the Bitcoin blockchain, and you just keep doing that every 10 minutes. That creates a history, and that’s why it’s called a block because you block all those transactions together and bolt them onto the last block.

POTENTIAL

Source: pwc.com

There are many potential applications for blockchain technology. It doesn’t necessarily have to be a cryptocurrency that you’re transacting in; it can be used for automotive systems, for example you could track different changes to your vehicle or updates or maintenance records.

For financial services, the technology allows for cheaper transmissions. So, sometimes you’ll hear that you can send money overseas for much cheaper from your phone to someone else’s phone using a cryptocurrency, for example. You don’t have to use Western Union or deal with some of the local authorities that are charging a lot in transaction fees.

Voting, you can track that.

Healthcare you can track records and so everyone who is given access can view these.

So, there is a lot of potential for block chain technology.

I would say, though, that it is very important to realize that the original reason for blockchain technology was very specific: it was to create a cryptocurrency or a digital unit of account that had some monetary value to it that people could trade amongst themselves and provide those benefits and really adopt to the digital age.

So previously, up to this point, you may say we’ve been in the information age and that’s where you have Google and other sources that basically provide you all the information you need very quickly are they’ve done that very efficiently.

CRYPTOECONOMICS

Now we’re looking at maybe the digitization age, and the question is, “how do you make everything digital, and to speed up access to records?”

And it’s creating something called crypto economics. I don’t hear this talked about all that much, and I think it’s because it’s a little complex. But what it means is, “how are you incentivizing the users?” So, if you use Facebook and you spent an hour on Facebook and post pictures, for example, what is Facebook doing? Well, they sell your information to an advertiser and that advertiser pays Facebook. You don’t benefit at all from that.

Here, in contrast, the idea is, “well, maybe we have a way to incentivize the users of the networks.” So, the owners of Facebook are shareholders, here the owners of the Bitcoin network are the Bitcoin owners or those that own the cryptocurrency. What Bitcoin did as the original cryptocurrency was basically launch a cambrian explosion of a variety of these projects thinking that this was the next wave and there’s a lot of different use cases that could come about.

You can see all of these pictured below, but there’s been thousands issued.

Source: Rare Altcoin

So these are maybe the top 100 cryptocurrencies made. Ethereum is the second largest cryptocurrency, for example. And some on his list aren’t even available today, but the point is, there’s several different ones, and they’re unique. Think of them as different stocks, or companies. But instead of companies, they are networks. They’re just different individuals from different computer systems coming together for a reason to participate in that network for whatever it happens to be, whatever they’re working on.

BITCOIN SUMMARY

So, to getting back to understanding Bitcoin as the first one, and to understand the entire cryptocurrency landscape you must understand Bitcoin by far. It’s unique.

Bitcoin was created in 2008 by an anonymous cryptographer named Satoshi Nakamoto. Now, that’s an alias, nobody knows who he is to this day. He wrote a whitepaper, and it was titled “Bitcoin Peer-to-Peer Electronic Cash.”

What he was saying in it was this: you take away any of the authorities, you take away the banking system, and now you have a unit, and you can transact digitally from one to another. What he was solving, in computer science, is called the Byzantine Generals Problem, which is, “how do you know that one digital item hasn’t been spent multiple times.” In other words, how do you validate that one out of one? And that’s what he worked on.

How do you validate those transactions that I just mentioned in terms of how much does Chris have, how much does Mark have? Can they send what they’re suggesting they can send? Do they actually own that amount? Well, blockchain technology is called, “proof of work.” That’s where a group of computers compete to try to validate that transaction that you just sent. So, you send the transaction to the network, a group of computers actually competes to solve really what’s a mathematical problem, but in some essence a lottery, where every ten minutes (and it’s designed this way from Bitcoin software) they allow a miner to solve that problem and then validate that transaction. They’re spending computer power to do that, and they’re competing with other computer networks to do that. So with that, they’re spending a lot of money on the energy that it takes to complete the task. You may ask, “why, what’s the incentive?” And it is because they get mining rewards.

Mining rewards are basically new Bitcoin or the issuance of new Bitcoin. That’s how new Bitcoin are minted, or new ones are put out into the system. That happens every 10 minutes, new Bitcoin are issued. What we’ll talk about it in a moment is how they really drive value by issuing new Bitcoin and scarcity.

Remember, it’s an open-source public permissionless immutable ledger.

CL: Hey Mark, before we go on to the next bit of information, about five years ago I had two separate clients, one had read a lot about Bitcoin and went out and bought his own computers, setup his own mining, and a couple of things he mentioned was a) the cost for the equipment was high, and the other thing was b) the cost for the electricity you need for the cooling that was necessary for the computer room he had built was expensive. The second client was a young man whose grandfather passed away and he got like $60,000 in an inheritance. He had gone out and did a very similar thing. My question is, when they’re competing, does buying state-of-the-art computer chips and optimizing speed give a miner a definitive advantage to somebody that might just setting up their laptop in thier office to run all the time, 24/7 but they’re still running DOS 3.0 from 20 years ago. Do you have any insight on that?

MD: I do. Originally, when it first launched, there wasn’t that many people mining because the mailing list for Nakamoto’s whitepaper on cryptography was very small. The reason for this was they didn’t realize what this ultimately would become. At that time, you could mine it on your computer in your home with a CPU chip. Then, as it got more competitive and it started to gain a little traction, you had to go up to the GPU, which is a graphics chip, a gaming chip. Now, these are becoming mining farms where it’s a warehouse full of computers just running and running. One of the major companies that provide the chips in video which is a major semiconductor maker is trying to produce the next generation type chips to help these miners. And miners do upgrade their equipment rather frequently to compete. And so, there’s big money in it now. It’s not something where you’re in your garage and running computers.

CL: So we’ve elevated past the bubblegum and the shoestrings. I got it.

MD: Yes, for sure.

CL: Ok, well thank you .

DIGITAL

Source: Medium.com

MD: I did want to talk about this picture above because I think it’s interesting. When you hear people talk about Bitcoin or cryptocurrency and act like it hasn’t been worked on or that there’s no background to this, it’s not the case. This was an issue, or a project has been worked on for 40 to 50 years. You had computer scientists really put time and effort into this project. Bitcoin’s creator was very familiar with almost all of these and references different features of different whitepapers or projects. So, Satoshi weaved these previous works into his whitepaper and noted that they each solved parts of the issue, and he connected the dots in a profound way. That essentially allowed a whole network to start building.

On the above timeline, all the way to the right, you see that Bitcoin was launched basically in 2009. So, the whitepaper was released in 2008, and the first transaction started in 2009 and the system started to build literally from the ground up.

Sometimes you may see those pictures of Bitcoin going from zero all the way up to its current price, and you may be excited by that. However, you can say that with a company, too, where it had zero value and then suddenly it went up a significant amount. So sometimes that value timeline of Bitcoin may be misleading. The reason for the increase was that just more and more people started to get involved and enjoy it. At first, they were really hobbyists that liked this idea and played around with it.

DECENTRALIZED

Source: Medium.com

Going back to the technology as it developed and blockchain technology from 2009, it really developed not only to use as kind of a method to transact in cryptocurrencies, but you could (since it’s a computer program) code it to include what are called smart contracts. In other words, you can code it in different manners and really make it whatever it is. And that goes to the use cases. It has some flexibility and that’s why you see so many different cryptocurrencies being launched. I would say that they are different than Bitcoin. Bitcoin is very specific; it is the first one. It’s almost like it’s the reserve of all the others that have come after it.

SCARCE

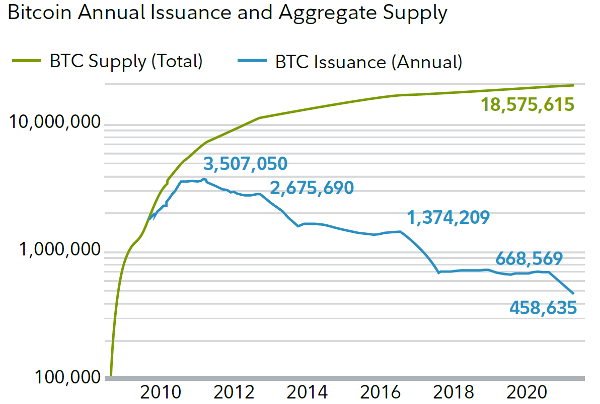

Source: Fidelity

I was mentioning above, there are mining rewards. So, how much Bitcoin do you get issued as a miner, and how much is available every 10 minutes?

Bitcoin was coded in such away where there will only be 21 million Bitcoin ever produced. At the time of the posting of this chart, there was 18.5 million (in that green line there) Bitcoin mined (available out there). There’s almost 19,000,000 today. What it started with was 50 Bitcoin. Every 10 minutes, 50 Bitcoin would be mined. It wasn’t very much money in the early days, but every four years the amount of Bitcoin and mining reward would be cut in half. So, it went from 50, to 25, to 12.5, and then 6.25.

What that’s done is really enforce this idea of scarcity. Less and less Bitcoin can be mined. So, for those proponents, they are saying “well it’s the first digital, decentralized (that means government doesn’t control it and it’s simply created and then the marketplace, the users, will determine its value based on market conditions, enthusiasm, availability, and other reasons why speculators may get involved or just users are transferring money that want to use the network for different reasons) currency.

But the scarcity component really tells you that there’s not going to be just an unlimited amount. That was one of the issues with digital assets, you just keep producing an unlimited amount, so in theory it would ultimately have minimal value. Now there are cryptocurrency’s that do have an unlimited amount, a lot of them do. Something that was popular last year was something called Dogecoin that ran up. That was a speculation kind of move in those marketplaces but I don’t think it was very well understood that Bitcoin is scarce, there’s only 21 million that will ever be available vs. Dogecoin where they’re just going to keep producing as many of those assets as they can, there is no cap. Therefore, there is no scarcity value.

CRIMINALS

Source: chainanalysis.com

Another issue that pops up is that criminals use Bitcoin. Or that it’s a criminal network. Well, it’s a public ledger. You may hear every so often that the FBI or the government has found somebody that illicitly used cryptocurrency and they arrested them. That’s because it’s a public blockchain, everything can be seen. It’s pseudonymous not anonymous, so everything can technically be tracked down if you’re doing something illegal. The illegal use is far below that of cash. That might surprise people, but it’s very minimal anymore.

Originally maybe you heard a story of something called “The Silk Road” which was way back circa 2012-ish where they basically created a website, and they sold some elicit or illegal things on there. It was kind of this trading route. It was just a website, but they did transact in Bitcoin. It really wasn’t Bitcoin in the sense of what it is today where now people know what it is, regulators know what it is. It’s a much bigger community that have been participating in Bitcoin now. So, this is one of those myths that are out that I don’t think really rings true anymore to the ecosystem.

PAYMENTS

Another thing I was alluding to at the beginning was payments. So, can you pay for your cup of coffee with Bitcoin or cryptocurrency? Well, one, if it’s Bitcoin and it’s scarce, you wouldn’t want to transact in Bitcoin. The other reason is, it’s not a payment system. Visa for example is a payment system. They can process 24,000 transactions a second. Bitcoin can do about 7. It’s not designed for those types of transactions. It’s designed to be secure, move slowly. I call it a settlement network, meaning if you’re moving larger sums or want to move those sums it’s not a payment network where you’re doing your everyday transactions. So, it would be foolish. And in the US, it’s not considered currency, so that would be a taxable transaction anyway – you have to record it and act like you sold it if you bought something with it. That’s not very well understood so you’ll hear that question probably for years to come in the media.

EMERGING ASSET CLASS

We think of this as an emerging asset class. It’s very early on. It’s different than equities or bonds. Cryptoassets are a different category and within cryptoassets there are different types of cryptocurrencies but understanding Bitcoin is crucial in order to understand the rest of the ecosystem. So, with equities you have corporate profits, economic growth, interest rates, productivity goes into those. With bonds you have economic growth, interest-rates, issuance, so they’re financial instruments. Cryptoassets are based on investor adoption – does the network grow overtime (meaning more users), how are regulators going to look at this, and will institutions start to participate in that asset class?

GOLD ALTERNATIVE

Source: winklevosscapital.com

A good way to look at Bitcoin, I think, as opposed to looking at as a currency like the US dollar, is to compare it to gold.

From a scarcity perspective, why is gold attractive? It scarce, it’s recognizable. Bitcoin’s supply is fixed; we know there’s going to be 21 million. We know the schedule Bitcoin will be produced. Gold is scarce, but we can get more of it if gold mining picks up. If gold prices go higher, usually they’ll start to try to mine more gold. Where with Bitcoin, that doesn’t work and that’s why you have these boom-bust cycles. If the price is going up, you just don’t find more Bitcoin.

Another difference is, it is software for Bitcoin but hardware for gold. Portability wise, Bitcoin you store in your phone, digitally. Gold is hard to move around, its heavy. As far as divisibility, Bitcoin can be divisible into basically the ninth decimal place, I believe. You can go very very thin. You don’t have to buy one full Bitcoin, which trades around $28,000. You can buy fractions of that, $25 worth for example, $30 worth, $100 worth. You’ll just get fractions in Bitcoin.

When it comes to storage, for Bitcoin it’s stored in a digital wallet. Very easy for Bitcoin. With gold it’s a safe or vault.

Counterfeiting – it’s very difficult with either.

Gold’s now about an 11 trillion-dollar market, Bitcoin’s about 800 billion, so there’s a big difference. Some of the proponents of Bitcoin will say, “well, it could catch gold,” it has some of the same properties where it goes up and down. It’s a very similar type of vehicle, except one’s digital and the other obviously is gold.

VOLATILITY

Source: @JurrienTimmer, Fidelity.

This is the rub with Bitcoin from an investor’s perspective: understanding the volatility of Bitcoin. Even though Bitcoin has grown over the last 10 years, it is as volatile as ever. If you look at a drawdown of 50%, that rarely happens in the S&P 500. 4% of the time, basically since 1900, it hasn’t done that. It’s just a few occasions. And that’s a major, major decline. With Bitcoin, 50% of its existence it has had a 50% decline. In other words, if you own Bitcoin you need to expect a 50% decline, and that’s a lot different than the S&P. In fact, we’ve just gone through a more than 50% decline from just a few months ago with Bitcoin. This happens pretty frequently. Typically the volatility level in Bitcoin is dramatic. Even a 70% decline almost a quarter of the time, it experiences that. So, it’s at a pretty frequent clip that this volatility may not be appropriate for everybody. But it’s OK to take a look if you have interest in it, and how to get access to it.

Does it make sense is an investment? For me, you have to go in expecting that 50% drawdown, maybe a four-year holding period before you even evaluate it. That market just moves around a lot. I don’t think that’s changing anytime soon, even if that network grows like it has been. That volatility will remain.

CL: So, before we go, because I see Fidelity there on the last chart, I heard on the news last week that they recently announced for folks that want to invest in crypto within their 401k that it will now be available. A couple thoughts cross my mind, one being volatility. As you know, with great reward comes great risk, as this chart identifies.

So, you have a couple things going on: people are hearing about it, now their corporate plans may offer it, so if the plan sponsor allows it, they’re able to step into an index. They invest in it. What’s your take on taxation? So, let’s just say you dollar cost average into it. If you look at Peter Thiel, that gives us the perfect example. He put all that money into a Roth, and it was just all tax free and the government looks at that and frowns upon that. So, if you could speak to that briefly, that would be insightful.

MD: Sure, if you’re looking for a long-term investment like this that has the potential to grow and a level of volatility you think of it as position sizing. Which means OK, it’s a small allocation, and then if it has an upside potential, what Peter Thiel did was he put it in a tax deferred account essentially, and a Roth, even better, where you’re not being taxed on those withdrawals. But in the 401(k), that makes sense, to put it away and just think of it as long-term money.

I mentioned four years, that would be kind of the minimum hold. So, in other words, if you think you’re coming in and just doing a short-term trade, I don’t know if it’s worth it because of the volatility. You’ll get swung around there. You could be very smart for the first three weeks then very foolish the next four weeks. And the numbers will be big, they won’t be small. And that’s why I say it makes sense if you’re putting it away. If you like it. And you don’t have to. It’s not for everyone. It’s not where it’s replacing the US dollar.

What it will do is give access to people that may have a cell phone in the third world country that doesn’t have a strong currency. It may give them access to get Bitcoin and then convert to the US dollar when they’re transacting business. That’s something that I think opens up a lot of possibilities for those in the emerging markets and economy to get access to US dollars. I don’t see the US dollar competing with Bitcoin, I think they actually will complement each other in that sense.

CL: Well Mark, I want to thank you. Really from the bottom my heart, I appreciate you. If anyone has questions, reach out to us.

MD: Thanks, Chris.

Investment Advisory Services offered through Retirement Wealth Advisors, LLC (RWA), a Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Insurance products and services are not offered through RWA but are offered and sold through individually licensed and appointed agents.

Annuity guarantees rely on the strength and claims-paying ability of the issuing insurer. Any references to protection benefits or lifetime income generally refer to fixed insurance products. They do not refer in any way to securities or investment advisory products or services. Fixed insurance and annuity product guarantees are subject to the claims-paying ability of the issuing company and are not offered by RWA.

Index or fixed annuities are not designed for short term investments and may be subject to caps, restrictions, fees and surrender charges as described in the annuity contract. Guarantees are backed by the financial strength and claims paying ability of the issuer.

Cryptocurrency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Cryptocurrency is not backed nor supported by any government or central bank. Cryptocurrency price is completely derived by market forces of supply and demand, and it is more volatile than traditional currencies and financial assets. Investing in cryptocurrency comes with significant risk of loss that a client should be prepared to bear, including, but not limited to, volatile market price swings or flash crashes, market manipulation, economic, regulatory, technical, and cybersecurity risks. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing. Volatility Risk: Cryptocurrency is a speculative and volatile investment asset. Investors should be prepared for volatile market swings and prolonged bear markets. Cryptocurrency can have higher volatility than other traditional investments such as stocks and bonds, and market movements can be difficult to predict. Economic Risk: The economic risk associated with cryptocurrency is in the lack of widespread or continuing cryptocurrency adoption. The market and investors could decide that cryptocurrency should not be valued at the current market capitalization due to a variety of factors. Regulatory Risk: Cryptocurrency could be banned or highly regulated by governments that would deter investors from buying or holding cryptocurrency. Technical Risk: Cryptocurrency is a dynamic network with a codebase that is updated to add new security and functionality features The updated code that is merged by the core developers could potentially have an error that threatens the security or functionality of the cryptocurrency network. Cybersecurity Risk: Cryptocurrency exchanges and wallets have been hacked, and cryptocurrency has been stolen in the past. This is a potential risk that clients must be comfortable with when investing and holding cryptocurrency. Theft is less likely when holding cryptocurrency at a qualified custodian in offline systems (cold storage) with institutional security and controls. Limited Operating History: Brookstone has a limited operating history in the cryptocurrency space upon which prospective clients can evaluate its performance. There can be no assurance that Brookstone’s assessment of the prospects of investments in crypto assets will prove accurate or that a client will achieve its investment objective.

Yesterday’s market was OK, it came roaring back, and today just we’re down 1000 points – we’ve gave back everything we gained yesterday and more.

I have been approached by a couple of clients that are getting to retirement age and are concerned.

We have talked for a while now about having strategies to defend against rising interest rates. So you have that, coupled with inflation, you’re going to create now what’s sort of a byproduct.

As much as I would like to say “hey, it’ll be fine, and there’s clear skies ahead,” I’m of the opinion that there’s choppy water ahead.

To what degree? I don’t know.

Now the other side of that is I am not a doom and gloom type of advisor. I’m pragmatic. And although I do understand turbulence, I also know that we can smooth that ride to a degree.

One way to do that is to incorporate a MYGA (Multi-Year Guaranteed Annuity) into your overall strategy. But first you have to understand what they are and how they can work.

I’d like to start with the Reader’s Digest definition of “annuity.” An annuity is really a promise that an insurance company will pay regardless of how long you live. And we’ll get deeper detail a bit later in this post but, the thing I wanted to outline here is longevity credits in annuities through a little story.

LONGEVITY CREDITS

Suppose five 90-year-old woman take a vacation together every year. The five women each place one hundred dollars in a box. Take that $100 and multiply it by five, and you have $500.

Now because they’re 90, unfortunately one of them passes away. So, the next year they leave for vacation but now there’s only four ladies left so they split the $500 they put in the year before and each woman now has $125. That’s a 25% rate of return.

The question is how much was invested in the market and what interest rate did it earn?

Nothing. Because they weren’t in the market.

Instead of using the money for vacation, the friends decide to let it ride. The next year, one more lady passes away. And now the 3 ladies return for vacation and split the $500 three ways, so they each get $167. That is a 67% return.

All of this is based on longevity credits or sometimes what is referred to as mortality credits. They weren’t in the market, the $500 didn’t increase, but they are each getting a return on their money since they’re splitting it among less friends.

In annuities, longevity credits are created when people die sooner than expected and don’t receive as many income payments as they would have if they had lived their full life expectancy. That money goes into a pool that will then pay lifetime income to those people who live longer than their life expectancy.

If you find yourself at the dinner table trying to explain this to somebody, life insurance pays if you die (so everybody pools their money together to pay a death benefit), annuities pay if you live (you’re still pooling your money together). If you end up being one of those people that make it to 100, 110, 120… the insurance company is on the hook to pay you as long as you’re alive.

GUARANTEED PAYMENTS FOR LIFE

With that being said, there are only three tools that can guarantee payments for life.

One of them, what I call a unicorn, is a pension.

The second one (a lot of people are in fear of going away) is Social Security. This is a promise from the federal government that they will pay you an income stream based on how much you contributed while working. A lot of people are fearful saying, “It’s not going to be there, it’s going to be bankrupt,” for most of us reading this, I don’t think we have any issues. For some of the younger generation, maybe the millennials, it will change, the rules will be different, but the money will be there.

Now the third option is an annuity and it’s important to note that there are several different types of annuities so it’s important to differentiate them. But we’ve all heard that commercial, “I hate annuities and you should too!” Well, there’s aspects that maybe aren’t attractive. BUT not every annuity has to be used in the same way. Not every tool is going to be utilized to do the same job.

I want to share a picture that can help you understand the different types of annuities.

IMMEDIATE ANNUITIES

The left side of the equation is what we call an immediate annuity. This is where you give up all control. You are trading an asset with the insurance company. You’re saying, “here’s my cash” and you can never get it back once you receive a payment option. This works just like a pension, so if you have ever seen pension statement where they say if you take X amount, you get 100% of Y, but if you want to make sure that you get at least a payment for 10 years (that’s the period certain) you’ll get a little bit lesser amount. Or if you want to make sure your spouse gets something (survivorship) then there’s even a lesser amount. Or you can get a combination of both.

Usually when you have a corporation that has a pension, or you have a municipality, or the federal government, or even a state government offering these types of products, they’re really just annuities with these terms. It’s based on actuarial data. This is NOT what we’re talking about today.

Here’s the main reason people don’t like immediate annuities: let’s say that you had $100,000. You go to the insurance company, and you say, “here’s $100,000, give me $80 a month for the rest of my life.” $80 being just an arbitrary number to keep the math simple.

You turn around and cash that first check for $80.

Would you agree that the insurance company still has the other $99,920? They have the balance of your money. It hasn’t gained interest. You only got paid one month.

Well, what happens when you have a bad day – you get hit by a bus?

The insurance company gets to keep your money.

This is why there’s a lot of negative press because nobody wants to exercise that risk. We don’t know how long we’re going to live.

Now some people may suggest that you can just take that money, invest it in the market, you can do better than what an annuity could do for you. The problem is, none of us know when we are going to die. That’s the trade-off.

I’m not here to sway your opinion one way or the other, I just want you understand how an immediate annuity works. When you start those payments, that’s called annuitization. That word means that you had given up control. It is an irrevocable agreement. You hand over your money and say to the insurance company, “here is my money, pay me, whether I live a day, I cash a check, or I live a month, or I live till I’m 120, you must pay me or my spouse for the rest of my life.

DEFERRED ANNUITIES

But we’re not focusing on immediate annuities today. We’re focused on deferred annuities. And there are different types of these as well.

The first is variable deferred annuities. If you know me, I don’t like an abundance of risk. This is what that commercial, “I hate annuities and you should too” is talking about.

You’re basically saying to an insurance company, “Here’s some money, I’m going to take all the investment risk (so you can lose money inside of it), and they’re expensive.

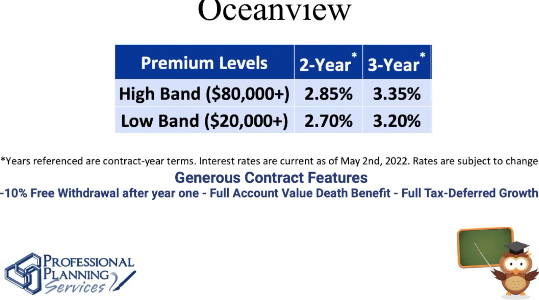

The type of annuity we utilize mostly is a fixed annuity. There are two different versions. Indexed Annuities (ie. Allianz 222 that I’ve talked about in the past that currently is offering a 35% bonus) or a Multi-Year Guaranteed Annuity. MYGAs are really the insurance company’s version of a bank’s CD. It’s for a (usually short) period of time. It’s guaranteed by the credit worthiness of the financial institution, which in my example to follow, happens to be Oceanview.

OCEANVIEW AND AM BEST RATINGS

Oceanview is rated A- (Excellent) by AM Best. Me and my advisers across the country are typically never going to use anything less than a A-. That’s just because that increases risk if an insurance company goes insolvent.

I get that question often. Just keep in mind that every insurance company is regulated by the state in which they do business. So, in New Jersey, it’s no picnic. In order for an insurance company to do business here in New Jersey, they must contribute to something called a Guaranty Fund. But not only are they putting in money just for themselves, but they also have to contribute for any other insurance company that does business in the state. They have each other’s backs. If you look at banks over the years compared to insurance companies, banks have defaulted at a much higher rate than insurance companies in the last 30 years. I’m much more comfortable with financial reserves required of insurance company to do business in the state versus what a bank is required to have.

But with that being said, the AM Best ratings are just benchmarks that we typically like to use. I don’t like to use B+ companies but depending on product options and needs of a client, once or twice I have deviated from my mainstream. But for purposes of this blog, I’m very comfortable with Oceanview’s financials.

Oceanview just had rate increases (See attached chart). And here’s their offer.

VOLATILE MARKETS

If you’re close to retirement and you’ve looked at the market today, you will you see that is down over thousand points and you may go, “Oh my God, I can’t take this anymore.”

Sidetracking a bit here, but when you see the market, and the markets down a thousand points, you must ask, which index is it? So maybe it’s the S&P maybe it’s the NASDAQ – tech sector’s been getting crushed. Are your holdings in that area? If you’re not matched up or mirrored identically, you’re likely not down equally in comparison to the market. Unless you’re in the S&P index. If you’re in the S&P index and the S&P lost 100 points, then yes, in fact, you should have lost pretty close to that. But if you’re looking at the DOW in the DOW is down 1000, well that’s only thirty stocks. So, you just have to put that in perspective.

Remember what I talked about before…the news networks like noise, and they need information to be able to spew, whether positive or negative, so they can generate emotional swings. That’s what gets ratings and people tuning in. Our job is to manage expectations, to help manage emotions and take a step back and to have a strategic plan.

So my thinking is, typically bonds are not an area that is going to do well on a go forward basis, in this rising interest-rate environment. I think everybody that is listening to the news will see that interest rates are going up. The fed just raised interest rates a half a point yesterday, the market liked it for a little while, and then went and slept on it and then didn’t like it today. That’s the equities market. Bond markets didn’t like it either.

So you turn around and go, “wow, my 60/40 portfolio lost money.” It’s going to be hard area of our portfolio to recover. I also don’t believe that we can time the market. You can’t sit here and go “get in, get out.” That has been proven. I don’t care who you, or how savvy you are, it cannot be done with any degree of predictability. However, you can take your winnings, or you can put in stop losses, or you can add a tactical component to your overall investment philosophy and that’s what I’m suggesting here.

UTILIZING A MYGA

If you’re feeling like you’ve had enough with the current volatility, utilizing a MYGA might be a solution for you. To use this strategy, you would have to have a 401(k) or IRA. If you own an IRA, you can do this. BUT if you own 401k, you need to check if they allow an in-service distribution or you’re over age 59 1/2 – either one of those things, you can this strategy.

Moving money from your retirement account to a MYGA means that you have a guarantee from insurance company that they are going to take your money, trustee to trustee (retirement plan to insurance company) put it in the tax environment of an IRA, and credit the funds a percentage based on the amount of money you contribute to the annuity. With this Oceanview product, you’ll see the minimum amount is $20,000 (between 20k to 80k) and they’ll give you 2.7% on a 2-year annuity. It’s not too bad. It beats a ten percent loss, 20% loss. Or on what MYGA companies refer to as a “high band” ($80,000+) it’s 2.85% for two years.

They have longer-terms, four years, five years, seven years… I didn’t get into all that because I think it’s a short-term solution to consider. A strategy to help give you peace of mind. I think a recession is still on the horizon …not tomorrow, not next month, not three months from now…but I do believe the next 12 to 24 months we will see that.

But if your money is locked up, and in 2-3 years you come out from underneath that, you can then take the money that you had in the MYGA plus the interest and put it back in the market. At that point the market should have settled down and we will probably be in a lower environment. That’s the thought process. If it’s something that you’d like to look at, send me an email or call the office and I will be in touch.

Investment Advisory Services offered through Retirement Wealth Advisors, LLC (RWA), a Registered Investment Advisor. Professional Planning Services and RWA are not affiliated. Insurance products and services are not offered through RWA but are offered and sold through individually licensed and appointed agents.

Annuity guarantees rely on the strength and claims-paying ability of the issuing insurer. Any references to protection benefits or lifetime income generally refer to fixed insurance products. They do not refer in any way to securities or investment advisory products or services. Fixed insurance and annuity product guarantees are subject to the claims-paying ability of the issuing company and are not offered by RWA.

Index or fixed annuities are not designed for short term investments and may be subject to caps, restrictions, fees and surrender charges as described in the annuity contract. Guarantees are backed by the financial strength and claims paying ability of the issuer.

College costs are continually rising and each year more and more of my clients are looking for creative ways to afford the kind of education they want their children to have – without leaving them with tens of thousands of dollars in high interest student loans. Even though a child could likely qualify for some type of financial aid including grants and scholarships or some type of work program, a large portion of the college tuition may still fall on the student’s and parent’s shoulders. An Indexed Universal Life insurance policy (IUL) can be a great way for parents to help pay for a child’s college education.

Why is the IUL such an attractive option? To understand what makes the IUL work for college savings, you first have to understand what an IUL is. The IUL is a permanent life insurance policy—meaning that the coverage will be in place as long as the policy holder lives and continues to pay the life insurance premium. A portion of the IUL is secured as a death benefit that will not change while a remaining portion is invested in an interest bearing account that can grow in cash value.

Typically, an IUL has an interest rate guarantee. This means that even if the index the insurer invests in performs poorly, the cash value portion of the policy will receive the minimum guaranteed interest rate. There are several different types of IUL policies including variable and fixed options. The cash value account can be used to pay for living expenses or used as funding for things such as a child’s college education.

Here are three reasons you may want to consider an IUL for education expenses:

Tax Advantages: The cash value portion of the IUL is tax-deferred as long as the policy stays funded. There are also instances when policy withdrawals from an IUL policy may be considered tax-free. If a withdrawal is made only on the money that is contributed to the cash value, then the withdrawal should be considered tax free. Loan distributions taken out on a cash value policy are also usually tax-free. However, the loan must be paid back over time or the death benefit will be reduced by the balance of the loan due.

Low Risk: An IUL may be used to pay for college expenses without taking away from the death benefit. A portion of the policy premium payment is going toward the cash value and another portion pays toward the death benefit part of your policy. The cash value will continue to earn a guaranteed minimum even if the index does not earn as expected. Your clients can have some peace of mind in not having to worry about market volatility.

Financial Aid: When the financial aid advisor determines the amount of financial aid to be awarded, assets will be calculated into that figure. The good news about the IUL is that life insurance normally is not counted as an asset in this calculation and won’t count against the assets in the analysis of determining the amount of financial aid received.

The cost of a college education is not going to be decreasing. In all likelihood, the cost of secondary education could continue to rise. The IUL works best toward college savings when looked at over the long-term. The idea is to allow the cash account to grow over the long-term and avoid withdrawing cash until the funds are needed to help pay for college. There may be a minimum cash balance requirement on an IUL that must be maintained to keep the policy in force. This will vary depending on the insurer. Overall, the IUL can be a great option to consider when looking at college funding options.

I’m not here to tell you how to live your life or how to manage your relationships. But I am a retirement specialist – and I can tell you that this article from Kiplinger makes some sense.

The basic premise discussed in the linked article is that while one partner may manage the money and make the financial decisions for the couple as a whole, when it comes to retirement planning, both partners should be involved.

Though out the years I’ve met many dynamic couples. I always request to initially meet with both spouses, as it’s important for me to learn about the individual goals so that we can determine what the couple’s combined goal may be. Oftentimes when a spouse doesn’t want to be involved, I have to discontinue discussions. I need everyone to be on the same page in order to understand the family’s goals.

I understand that couples may have goals that differ from eachother – and that’s fine. That’s perfectly normal in fact. But let’s face it, as the Kiplinger article states, one spouse is going to die before the other. It’s just fact. That’s why it’s important that everyone has a say in retirement planning.

Money can often be a source of tension in relationships. Believe me, my conference room has turned into a therapist’s office at times. However, finding a way to talk about money to each other is extremely important. Otherwise, you can find yourself at retirement age without enough money, or worse yet, widowed and completely shocked by your financial state.

If you’re having trouble talking to your spouse about money, my suggestion would be to go see your financial planner. Talk it out with someone who knows money, knows retirement, and who you feel comfortable with. Sometimes having an expert there helps ease the tension and can help get you on the right track to retire.

How many of you have heard this phrase or said it yourselves: “What’s the point in learning this math equation when it has absolutely no application in real life?”

I know I’ve heard it before. I’m the parent who helps the kids with the math homework. I’ve heard this from my eldest children and I’m sure I’ll hear it from my little girls at some point, too.

I found this article to be thought provoking preceding the weekend, because I’m a big advocate for making your children’s lives better than your own. Everything my parents gave me I will always be thankful for. They worked hard and provided wonderful things for me, and I am the man I am today because of that. I intend to make sure my children have a good start in life as well.

In the article, Ted Beck writes about how our grandparents learned all about personal finance in high school, while our children’s education is focused on college prep these days. He says, “high school’s endgame changed after 1945, an unintended consequence of the GI Bill. Math detoured from preparing young Americans to enter financial adulthood to preparing them to enter college. Money basics gave way to the college prep track: algebra, geometry, trigonometry, calculus.”

Now don’t get me wrong, I’m sure the number of teachers who try to incorporate personal finance lessons into their curriculum probably exceeds those who chose not to, but why are our young adults often financially illiterate? The problem is not the teachers (who in my opinion are god sends), it’s the SYSTEM and the BUSINESS of school. We’re funneling our children into higher education without fully preparing those who chose not to go to college. We have a broken education system.

So my point here is, as parents (or aunts/uncles/cousins/friends etc) we need to do our best to fill the gap the system is creating. We need to be the teachers – and not just when it comes to solving that math problem our 10 year old is stuck on (or someone elses’ 10 year old as we recently saw on the news) — but by teaching our children life lessons on personal finance. By being educated ourselves about the options out there to create and preserve our wealth.